Mortgage Rates in Q1 2026: What Buyers and Homeowners Should Know Right Now

In the current 2026 financial climate, the "one-size-fits-all" approach to mortgages is obsolete. Successful borrowers are those who leverage specific loan programs tailored to their financial profile. One of the biggest trends we are seeing this quarter is the resurgence of the Adjustable-Rate Mortgage (ARM). Unlike the risky products of the past, modern ARMs offer a fixed rate for an initial period (often 5, 7, or 10 years) typically lower than the standard 30-year fixed rate. For buyers who plan to move or refinance within that timeframe, an ARM can result in significant monthly savings.

However, the 30-year fixed-rate mortgage remains the gold standard for stability. For families planning to put down roots in Marietta for th e long haul, locking in a fixed rate now provides protection against future economic fluctuations. It is important to remember that mortgage rates are influenced by bond markets, specifically the 10-year Treasury yield. When economic reports regarding jobs or inflation are released, rates can jump or drop within hours. This is why working with a local expert like Jason Waters is essential—we can help you navigate the "float down" options or secure a rate lock before the market moves against you.

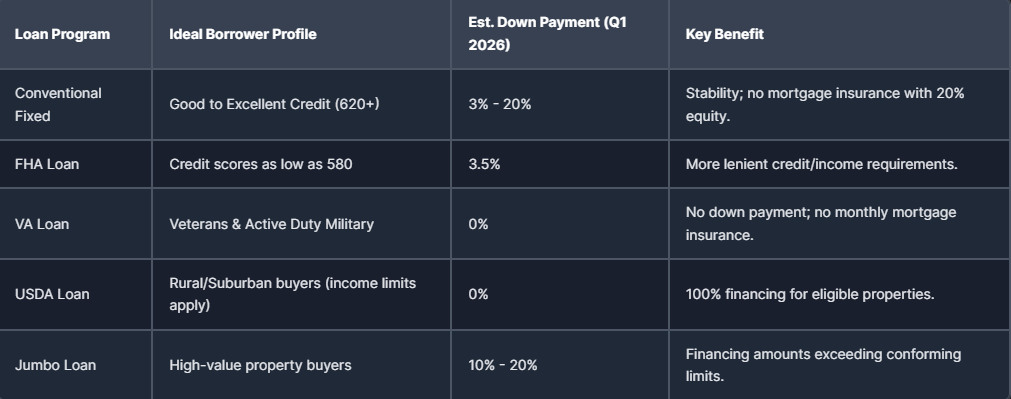

Furthermore, government-backed loans continue to be a pillar for many buyers. FHA loans remain a fantastic option for those with lower credit scores or smaller down payments, while VA loans offer unbeatable benefits for our eligible veterans in Georgia. In 2026, loan limits for these programs have adjusted to keep pace with home price appreciation, allowing buyers to finance more without moving into "jumbo loan" territory. Understanding the specific requirements and benefits of these programs can make the difference between a rejected application and a clear-to-close.

We also cannot ignore the impact of credit scores on the rates offered in Q1 2026. Lenders have refined their risk models, and the spread between the rate offered to a borrower with a 760 credit score versus a 660 score can be substantial. Part of our service at Affinity Home Lending involves helping you analyze your credit profile and identifying quick wins to potentially boost your score before application, ensuring you qualify for the most competitive rates available.