Breaking the 20 Percent Down Payment Myth

If you are dreaming of purchasing a home in Marietta, Georgia, you might be wondering how much cash you actually need upfront. For decades, the golden rule of real estate was that you needed a 20 percent down payment. However, as we move into 2026, that outdated advice is keeping too many potential buyers on the sidelines.

At The Jason Waters Lending Team, we want to clear the air. There are numerous flexible mortgage options available today that require significantly less cash out of pocket. Whether you are a first-time homebuyer or looking to upgrade to a larger property in Cobb County, understanding your choices is the first step to securing your dream home.

- FHA Loans: Great for buyers with less-than-perfect credit.

- VA Loans: Exceptional benefits for our honored veterans and active military.

- USDA Loans: Perfect for specific rural or suburban areas.

- Conventional Loans: Highly flexible options starting with very low minimums.

Let us explore exactly what to expect from the housing market and your down payment options this year.

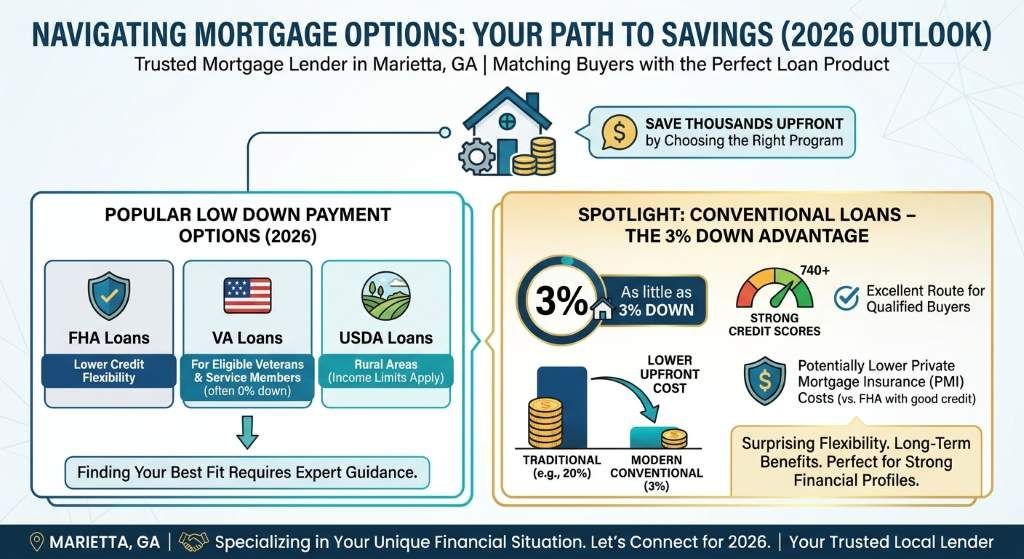

The Best Low Down Payment Mortgage Programs for 2026

Choosing the right mortgage program can save you thousands of dollars upfront. As a trusted mortgage lender in Marietta, GA, we specialize in matching buyers with the perfect loan product for their unique financial situation.

Here is a closer look at the most popular low down payment options for 2026:

- Conventional Loans: Many buyers are surprised to learn that conventional loans can require as little as 3 percent down. This is an excellent route for buyers with strong credit scores who want to buy a home in the Marietta area.

- FHA Loans: Backed by the Federal Housing Administration, these loans require just 3.5 percent down. They are incredibly popular among first-time buyers because of their flexible credit requirements.

- VA Loans: If you are an eligible veteran or active duty service member, you can purchase a home with zero down payment. This is one of the most powerful lending benefits available today.

- USDA Loans: For those looking at properties in eligible rural or suburban areas outside the immediate city center, USDA loans offer a 0 percent down payment option.

By exploring these flexible home financing options, you can keep more money in your savings account for home improvements, furniture, or emergency funds.

| Loan Program | Minimum Down Payment | Typical Minimum Credit Score | Mortgage Insurance Required? |

|---|---|---|---|

| Conventional Loan | 3% to 5% | 620 | Yes (if under 20% down) |

| FHA Loan | 3.5% | 580 | Yes (MIP) |

| VA Loan | 0% | No official minimum (often 620) | No (Funding Fee applies) |

| USDA Loan | 0% | 640 | Yes (Guarantee Fee) |

How The Jason Waters Lending Team Can Help You Succeed

Navigating the Marietta real estate market requires a knowledgeable partner. At The Jason Waters Lending Team powered by Affinity Home Lending, we are committed to providing you with expert advice and tailored financing solutions.

We understand that saving for a house can feel overwhelming. That is why we take the time to review your financial profile and help you leverage local down payment assistance programs, gift funds, and competitive loan products. Whether you are eyeing a historic home near Marietta Square or a modern build in Cobb County, we have the tools to get you to the closing table.

Compliance Notice: All loans are subject to credit and property approval. Program terms and conditions are subject to change without notice. The Jason Waters Lending Team powered by Affinity Home Lending, NMLS: 623984.

Ready to find out exactly how much you need to buy your dream home? Apply online today to get a customized estimate and pre-approval.

Q1: Can I buy a house in Marietta with no money down?

Yes, if you qualify for a VA loan or a USDA loan, you can purchase a home with a zero percent down payment.

Q2: Is it better to put 20 percent down if I have the cash?

Putting 20 percent down eliminates the need for private mortgage insurance (PMI) and lowers your monthly payment. However, keeping some cash on hand for emergencies or renovations might be a smarter financial move depending on your goals.

Q3: Can I use gift money for my down payment?

Absolutely. Most loan programs allow you to use funds gifted by a family member to cover part or all of your down payment, provided you have a proper gift letter.

Q4: What is the minimum credit score for a 3.5 percent down FHA loan?

Generally, you need a minimum credit score of 580 to qualify for the 3.5 percent down payment advantage on an FHA loan.

Q5: How do I know which loan program is best for me in 2026?

The best way to determine your ideal loan program is to speak with an experienced mortgage professional. Our team will evaluate your credit, income, and goals to recommend the perfect fit.