Planning Your Mortgage for 2026: Insights from a Local Expert

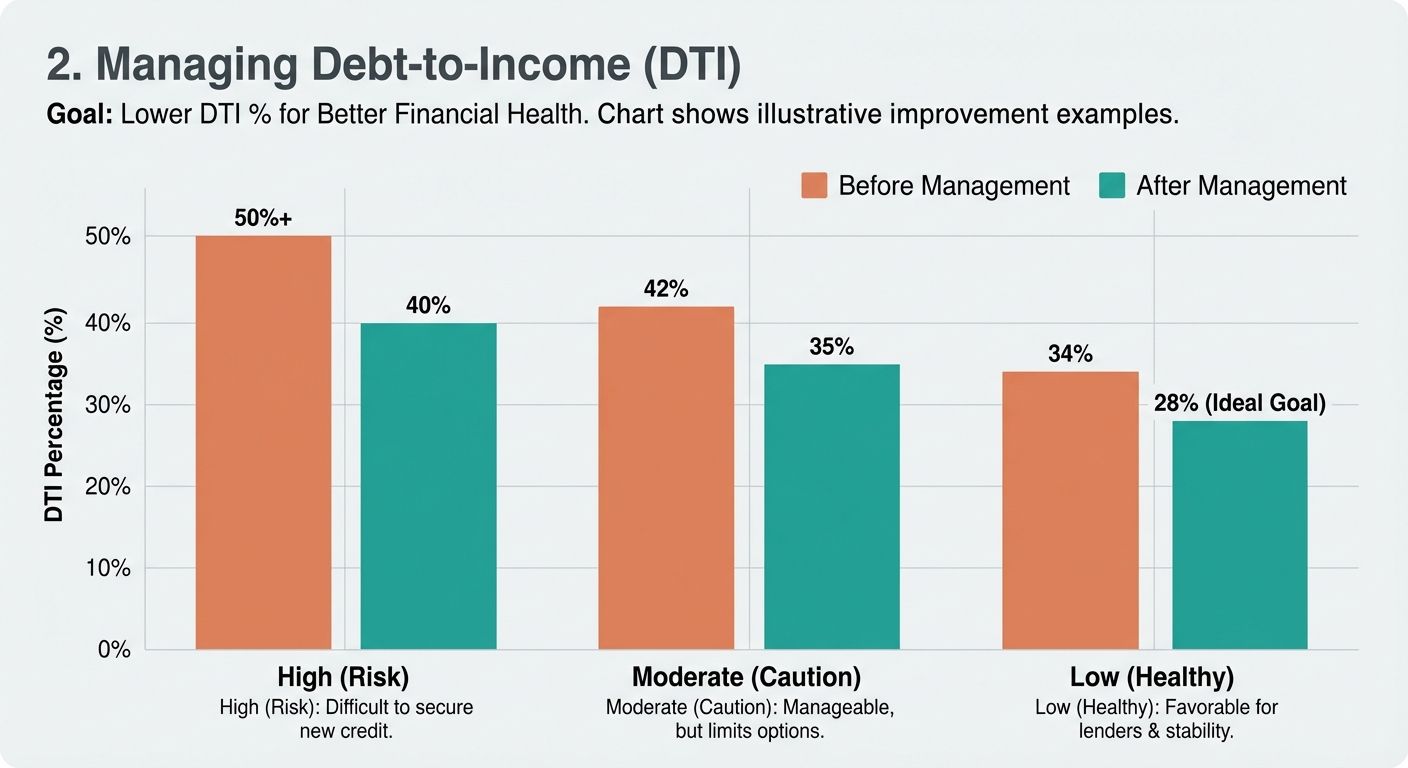

Strategy: If you are planning to buy in 2026, avoid taking on new large debts (like a new luxury car payment) right before applying. If you have a bonus coming up, consider using it to pay off a

high-payment installment loan to free up monthly cash flow, thereby increasing your borrowing power.

1. Strategic Down Payment Savings

A common myth is that you need 20% down to buy a home. This is false. However, your down payment strategy depends on your goals.

• 3% - 3.5% Down: Great for first-time buyers using Conventional or FHA loans to get into the market sooner.

• 20% Down: Ideal for eliminating Private Mortgage Insurance (PMI) and lowering monthly payments.

• Gift Funds: Many loan programs allow family members to gift funds for the down payment. We can help you document this correctly.

2026 Interest Rate Projections & What They Mean for You

The "Date the Rate, Marry the House" Philosophy:

If you find the perfect home in Marietta in 2026, do not let the interest rate scare you away. Home prices generally rise over time. You can always refinance your mortgage if rates drop significantly in the future, but you cannot go back in time to buy the house at today's price. The Jason Waters Lending Team specializes in refinance monitoring, meaning we will alert you the moment it makes financial sense to refinance your loan.

Loan Options to Consider in 2026

Choosing the right loan program is just as important as getting a good rate. Different programs serve different financial profiles. Here is a comparison of what might be available to you:

The "Jason Waters" Difference: Local vs. Big Bank

In the digital age, it is tempting to click a button on a massive aggregate website and hope for the best. However, real estate transactions in Georgia have strict deadlines and specific nuances. Here is why partnering with a local broker like Jason Waters at Affinity Home Lending makes a difference:

• Accessibility: You are not just a file number. You can call or text us at 404-850-9555 and get a real human being.

• Local Reputation: Listing agents in Marietta know the Jason Waters Lending Team. When they see a pre-approval letter from us, they know the deal is solid and likely to close on time. This can be the tie-breaker in a multiple-offer situation.

• Broker Advantage: As brokers, we shop dozens of lenders to find the specific product that fits your needs, rather than trying to fit you into a single bank's box.

Step-by-Step 2026 Mortgage Checklist

Ready to get started? Use this checklist to stay on track for your 2026 home purchase:

1. Q1 2026: Pull credit reports and dispute errors. Establish a savings plan for your down payment and closing costs.

2. Q2 2026: Connect with the Jason Waters Lending Team for an initial consultation. We will calculate your buying power based on current rates.

3. Q3 2026: Gather documentation (W2s, tax returns, bank statements). Get formally pre-approved.

4. Q4 2026: Begin house hunting with a trusted local real estate agent. Make offers with confidence knowing your financing is secure.

Frequently Asked Questions (FAQs)

1. How early should I get pre-approved before buying a home in Marietta?

We recommend starting the conversation at least 3 to 6 months before you intend to buy. This gives us time to identify any credit issues or income gaps and correct them. However, a formal

pre-approval is typically good for 60 to 90 days. If you are ready to look at homes immediately, we can expedite the process.

2. What is the difference between pre-qualification and pre-approval?

Pre-qualification is an estimate based on self-reported information—it gives you a general idea of what you can afford. Pre-approval is a verified commitment from a lender based on documented income and credit. In the competitive Marietta market, sellers require a pre-approval letter to take your offer seriously.

3. Can I buy a house in Cobb County if I am self-employed?

Absolutely. Self-employed borrowers are a specialty of ours. While traditional banks may struggle with complex tax returns, we have access to "Bank Statement Loans" and other non-QM products that analyze your cash flow rather than just your net income on tax returns.

4. How much are closing costs in Georgia?

Closing costs in Georgia typically range from 2% to 5% of the purchase price. This includes lender fees, title insurance, government recording fees, and prepaid items like property taxes and homeowners insurance. During our consultation, we provide a "Loan Estimate" detailing these costs so there are no surprises.

5. Do I really need a 20% down payment to avoid PMI?

While 20% down eliminates Private Mortgage Insurance (PMI), it is not a requirement to buy. Many buyers purchase with 3% to 5% down. Furthermore, if you have good credit, PMI can be surprisingly affordable. We can run a "cost of waiting" analysis to see if it makes more sense to pay PMI now and build equity, rather than waiting years to save 20%.

Ready to Build Your 2026 Mortgage Roadmap?

The path to homeownership in Marietta doesn't have to be confusing. Whether you are looking to buy your first home, upgrade to a larger space for your growing family, or invest in real estate, the Jason Waters Lending Team is here to guide you every step of the way.

Don't leave your financial future to chance. Let's build a plan that works for you. Contact Jason Waters today:

Phone: 404-850-9555

Email:

jwaters@affinityhomelending.com

Website:

www.jasonwaterslendingteam.com

The Jason Waters Lending Team powered by Affinity Home Lending. NMLS: 623984. Equal Housing Lender.